In this section we propose an approach, traditionally used in stock market, to model the returns of the price of Bitcoin.

1 Dataset

Dataset

pair ="BTCUSDT"from ="2018-01-01"to ="2023-11-20"# ohlcv data from binance df <-db_klines_binance(pair = pair, api ="spot", interval ="1d", from = from, to = to, dir = dir_db_crypto)# select only close price df_fit <- dplyr::select(df, date, Pt ="close") # close price# add time index df_fit$t <-1:nrow(df_fit)

2 GARCH(1,1) model

We start with a GARCH(1,1) to model the log-returns. Denote as \(P_t\) the close price at time \(t\), then define the log-close price simply as: \[S_t = \log(P_t)\]

Log-price

# compute log-price df_fit$St <-log(df_fit$Pt)

The log-returns at time \(t\), namely \(r_t\) are defined as: \[r_t = S_t - S_{t-1}\]

Under a GARCH(1,1) model the log-returns are parametrizated as follows: \[r_t = \sigma_t \epsilon_t\] where the variance is compute by the recursion: \[\sigma_t^2 = \omega + \alpha_1 r_{t-1}^2 + \beta_1 \sigma_{t-1}^2\] Note that, it is possible to come back to the close prices \(P_t\) by inversion: \[S_t = S_{t-1} \sigma_t \epsilon_t \quad \Rightarrow \quad \log(P_t) = \log(P_{t-1}) \sigma_t \epsilon_t\] Finally the close prices \(P_t\) are given by: \[P_t = P_{t-1} e^{ \sigma_t \epsilon_t}\] By substituting the values of \(P_{t-1}\), we obtain: \[\begin{aligned} P_t & {} = P_{t-2} e^{(\sigma_{t} \epsilon_{t})+(\sigma_{t-1} \epsilon_{t-1})} = \\

& = P_{0} e^{\sum_{i=1}^{t} \sigma_{i} \epsilon_{i}} \end{aligned}\]

3 Example: Standard GARCH(1,1) with Normal Residuals

Example setup

# Fit date date_fit_from <-"2021-01-01"date_fit_to <-"2023-08-31"# Simulation dates date_sim_from <-as.Date("2023-09-01")date_sim_to <-as.Date("2023-11-01")

GARCH(1,1) fit

df <- dplyr::filter(df_fit, date >=as.Date(date_fit_from) & date <=as.Date(date_fit_to))# Garch specification spec <-ugarchspec(variance.model=list(model="sGARCH", garchOrder=c(1,1)),mean.model=list(armaOrder=c(0,0), include.mean=FALSE),distribution.model="snorm")# Garch model fit fit <-ugarchfit(data = df$rt, spec = spec, out.sample=0)df_coef <- dplyr::tibble(x1 =coef(fit)[1], x2 =coef(fit)[2], x3 =coef(fit)[3])df_coef <-round(df_coef, 4)colnames(df_coef) <-c("$$\\omega$$", "$$\\alpha_1$$", "$$\\beta_1$$")knitr::kable(df_coef, escape =FALSE)%>% kableExtra::kable_styling(latex_options =c("scale_down"), font_size =6, full_width =FALSE)

$$\omega$$

$$\alpha_1$$

$$\beta_1$$

0

0.07

0.9048

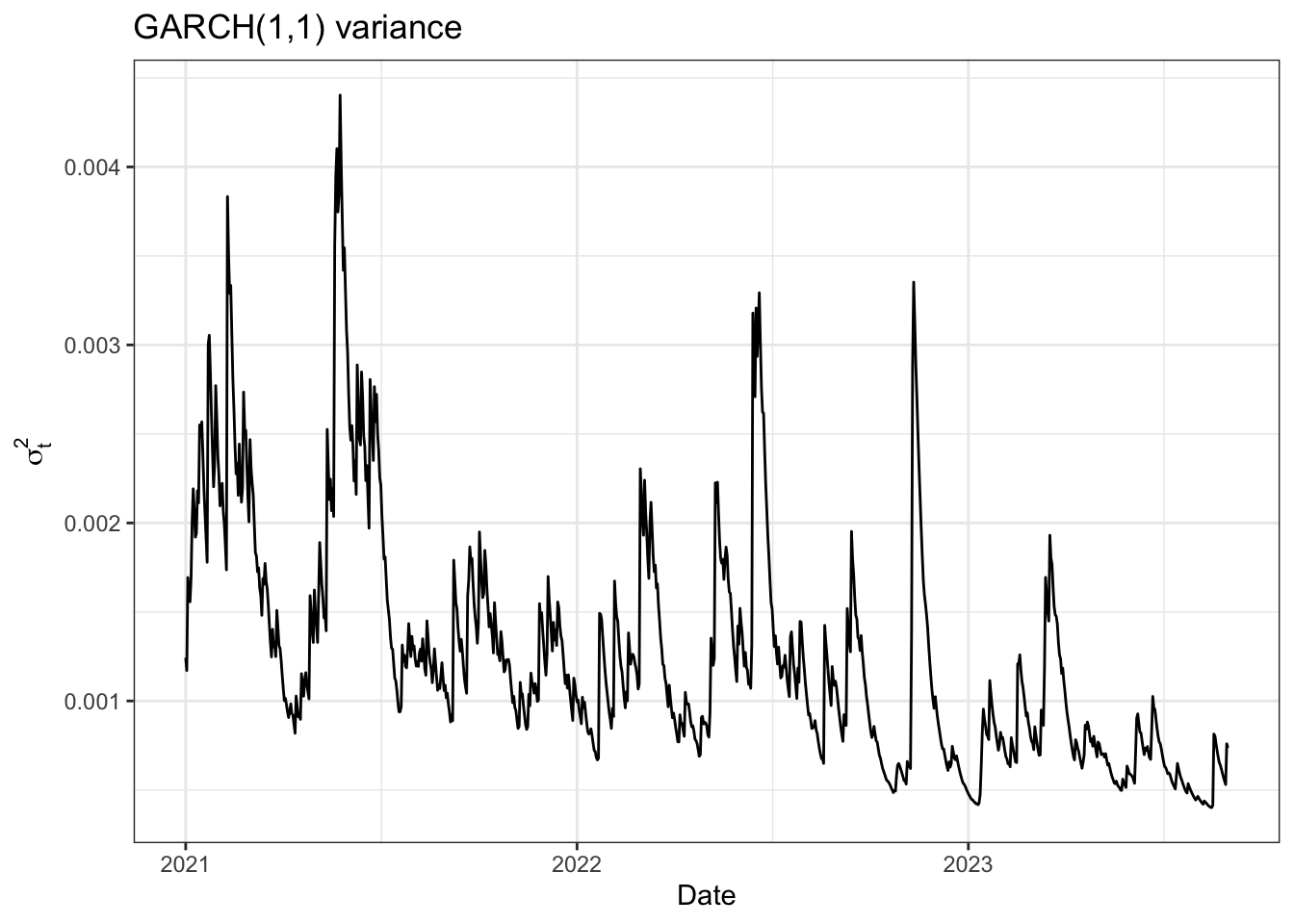

GARCH(1,1) variance

dplyr::tibble(t = df$date, sigma = fit@fit$var) %>%ggplot()+geom_line(aes(t, sigma)) +theme_bw()+labs(title ="GARCH(1,1) variance", y =TeX("$\\sigma_{t}^{2}$"), x ="Date")

4 Simulation of BTCUSD data

GARCH(1,1) simulations

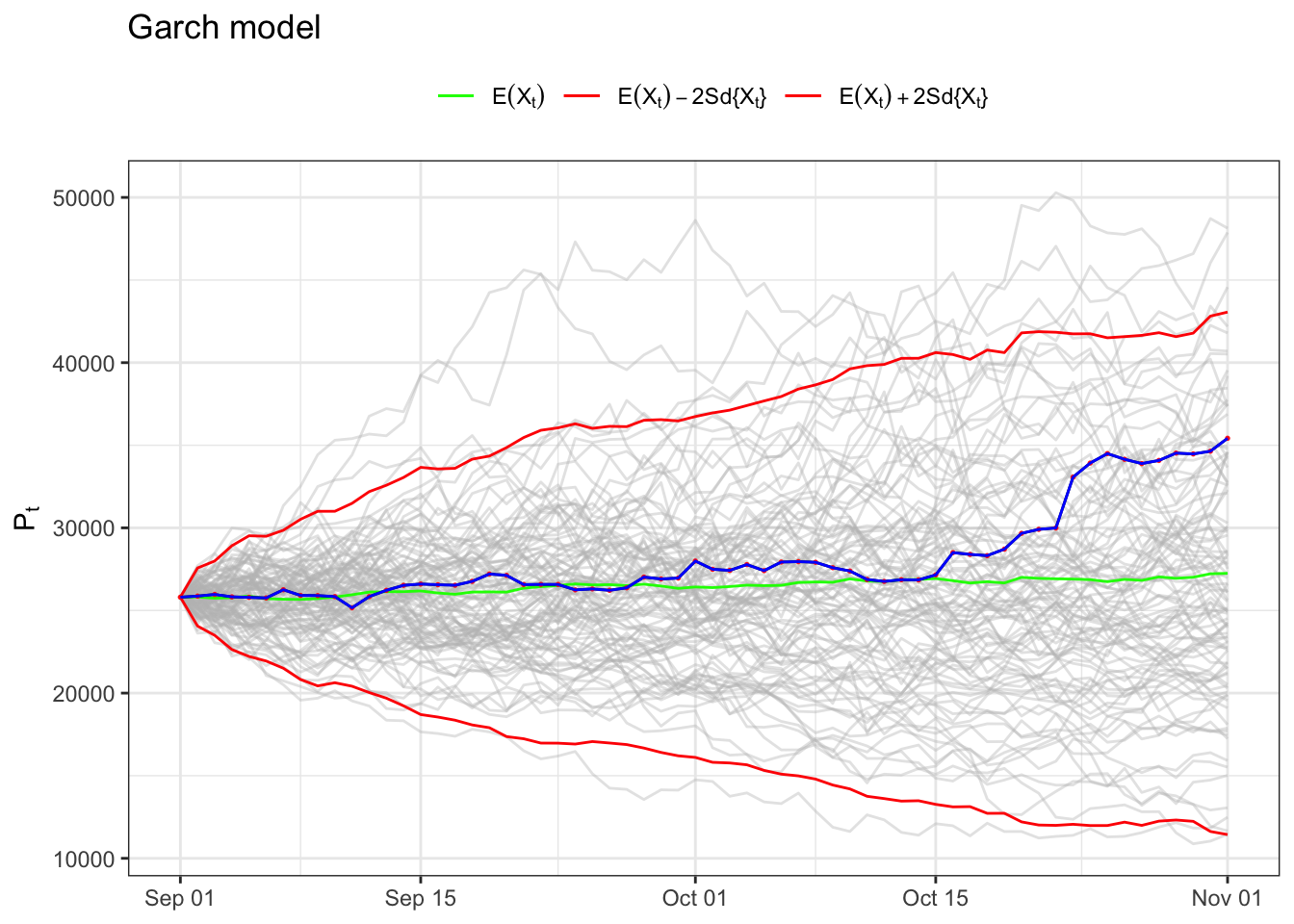

################### inputs ################### j_bar <-100# number of simulations seed <-1##############################################set.seed(seed)df_ <- dplyr::filter(df_fit, date >=as.Date(date_sim_from) & date <=as.Date(date_sim_to))df_$t <-1:nrow(df_)S0 <- df_$Pt[1] # initial price nsim <-as.numeric(difftime(date_sim_to, date_sim_from))# Garch model simulationssim <-ugarchsim(fit, n.sim = nsim, m.sim = j_bar)sim_ls <-list()for(i in1:j_bar){ St <- sim@simulation$seriesSim[,i] Sigma <-c(sim@simulation$sigmaSim[,i][1], sim@simulation$sigmaSim[,i]) sim_ls[[i]] <- dplyr::tibble(seed = i,t =1:(length(St)+1), St =c(0, St), Pt = S0*cumprod(exp(St)),Sigma = Sigma)}# dataset with simulations df_sim <- dplyr::bind_rows(sim_ls)df_sim <- dplyr::left_join(df_sim, dplyr::select(df_, t, date), by ="t")# dataset with mean path and standard deviations df2 <- df_sim %>%group_by(date) %>%summarise(EX =mean(Pt), Upper = EX +2*sd(Pt), Lower = EX -2*sd(Pt), e_sigma =mean(Sigma), sigma_dw =mean(Sigma) +2*sd(Sigma), sigma_up =mean(Sigma) -2*sd(Sigma)) ggplot() +geom_line(data = df_sim, aes(date, Pt, group = seed), color ="gray", alpha =0.4)+geom_line(data = df2, aes(date, EX, color ="expectation"))+geom_line(data = df2, aes(date, Upper, color ="upper"))+geom_line(data = df2, aes(date, Lower, color ="lower"))+geom_line(data = df_, aes(date, Pt), color ="black", alpha =0.9)+geom_point(data = df_, aes(date, Pt), color ="red", alpha =0.9, size =0.3)+geom_line(data = df_, aes(date, Pt), color ="blue", alpha =1)+scale_color_manual(values =c(upper ="red", lower ="red", expectation ="green"),label =c(upper = latex2exp::TeX("$E(X_t) + 2Sd\\{X_t\\}$"),lower = latex2exp::TeX("$E(X_t) - 2Sd\\{X_t\\}$"),expectation = latex2exp::TeX("$E(X_t)$")))+labs(title ="Garch model", x =NULL, y = latex2exp::TeX("$P_t$"), color ="")+theme_bw()+theme(legend.position ="top")

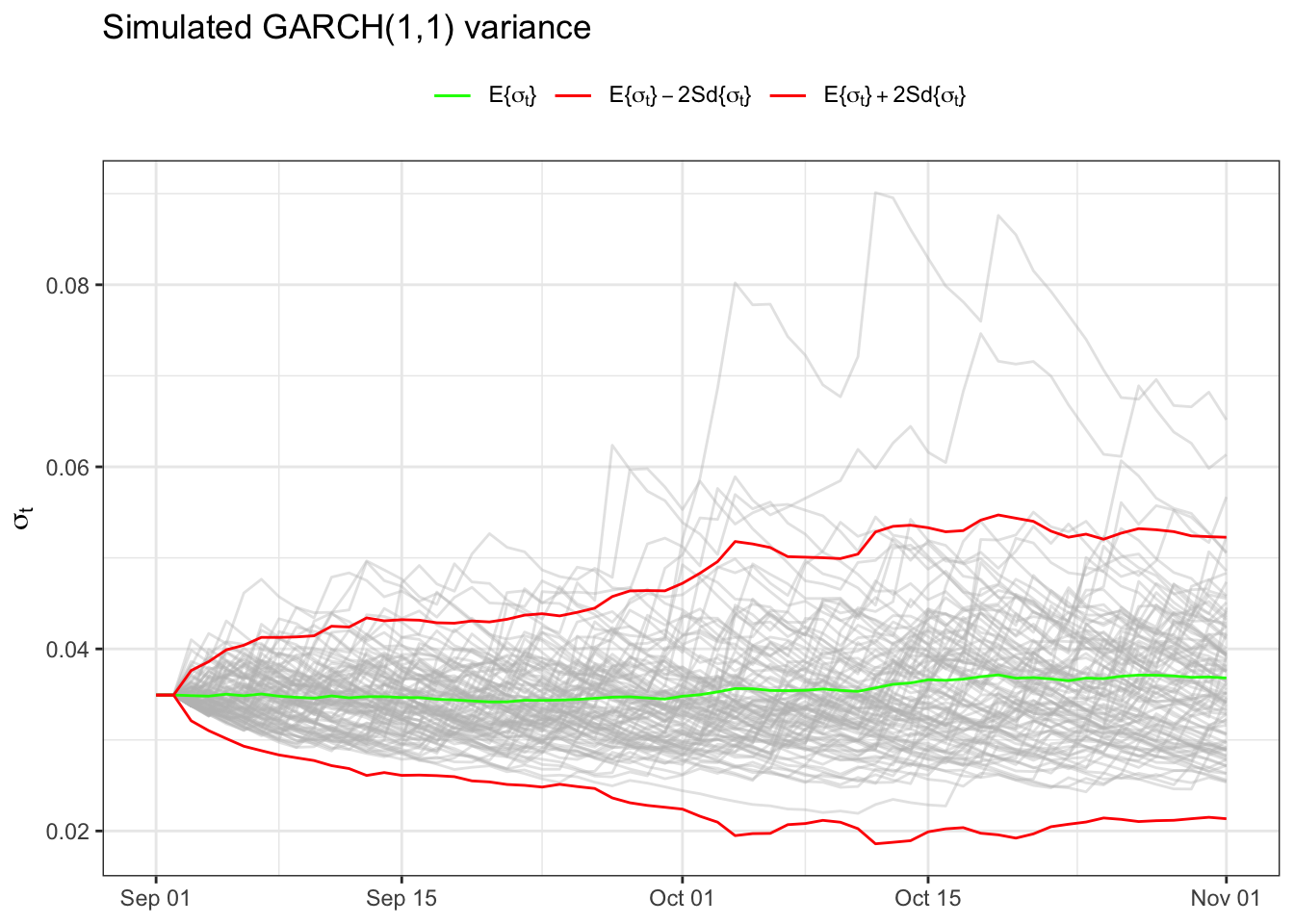

ggplot() +geom_line(data = df_sim[-1,], aes(date, Sigma, group = seed), color ="gray", alpha =0.4)+geom_line(data = df2, aes(date, e_sigma, color ="expectation"))+geom_line(data = df2, aes(date, sigma_dw, color ="upper"))+geom_line(data = df2, aes(date, sigma_up, color ="lower"))+scale_color_manual(values =c(upper ="red", lower ="red", expectation ="green"),label =c(upper = latex2exp::TeX("$E\\{\\sigma_t\\} + 2Sd\\{\\sigma_t\\}$"),lower = latex2exp::TeX("$E\\{\\sigma_t\\} - 2Sd\\{\\sigma_t\\}$"),expectation = latex2exp::TeX("$E\\{\\sigma_t\\}$")))+theme_bw()+theme(legend.position ="top") +labs(title ="Simulated GARCH(1,1) variance", y =TeX("$\\sigma_{t}$"), x =NULL, color =NULL)